Beware the Bearer Of BOE

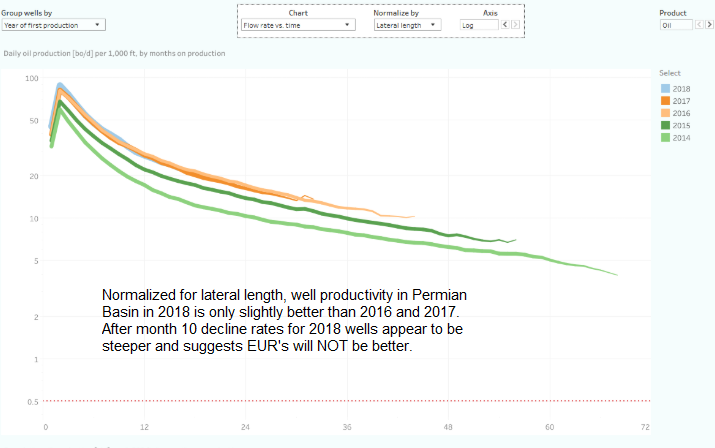

When normalized for lateral length there is a lot of realized production data from Permian Basin unconventional HZ wells, filed of record with the Texas Railroad Commission, that suggests oil productivity has not improved significantly since 2016 and may actually be plateauing.

Click to enlarge; shaleprofile.com, OSB text

Rystad Energy takes issue with this claim so in a recent October 2019 press release it argues that Permian Basin "productivity" per well continues to increase thru July 2019; its chart clearly shows that, below.

How can Rystad say that? It uses the miracle of barrels of oil equivalent (BOE) and includes associated gas in its analysis, that's how; 6 mcf of gas = to 1 barrel of oil.

BOE is basically, bunk. When used to estimate the economic performance of a shale oil well, BOE at a ratio of 6:1 is misleading as hell. Currently the price of WTI is $55.63 per BO and the price of natural gas at Henry Hub in Louisiana is $2.69; on a "value" basis (what else is there?) the BOE ratio should then be 20.6 mcf per 1 BO.

In the Permian Basin, however, the price of natural gas at its primary sales reference point, its 'hub," called WAHA, is currently (11.1.19) about 60 cents. That would make the BOE ratio something like 93:1. So, the gas in West Texas is worth pretty much nothing and they flare the snot out of the stuff out there. What good are British Thermal Units if they are getting burned off into the atmosphere?

Analyzing the future of shale oil in the Permian Basin, using BOE as a metric, is confusing and, at 6:1 ratios, meaningless. The Permian shale oil industry says associated gas can cover the incremental cost of lifting the barrel of oil out of the ground...I don't buy that, particularly not now with gas prices as low as they are and given the incredible amount of flaring going on in W. Texas. Incremental lift costs per barrel of oil is increasing, I believe, because of produced water disposal costs in the Permian. Those costs will eventually get very high. Some estimate the Permian Basin will be producing 35MM BWPD in five years. You are not going to BELIEVE what getting rid of all that shit is going to do to late-life economics.

Natural gas liquids (NGL's) stripped out of the associated gas stream do have monetary value, for sure, but not enough for me to want to mess with in my roughneck analyses.

If you want to understand the future of shale oil sustainability in America, not associated gas sustainability, check the BOE bullshit at the door. Here's an example of why...

Click to enlarge; shaleprofile.com, OSB text

Rystad's chart shows well "productivity" still increasing in the Permian Basin. The chart, above, is from Shale Profile Analytics and shows that the Permian Basin is definitely getting gassier every year, its gas to oil ratios (GOR in mcf/bo) constantly increasing.

So, the gassier the Permian Basin gets, the more 'e' there is in BOE. Initial potential (IP) of wells reported in BOE give people goosebumps. And, if well decline is a function of BOE then as GOR increases the well's implied decline rate is lessened, significantly. One part of the production stream is declining (oil), the other part of the production stream (gas) is increasing 6 fold.

Gas requires little operating expenses to produce; BOE at 6:1 ratios, can be used to dilute "lift" costs to get the good stuff (oil) out of the ground, significantly. A few years ago Pioneer blabbered its incremental lift costs in the Midland Basin were $2.00 per incremental BOE. That's an 'E' in fine print; its actual lift costs per BO are closer to $7.00.

BOE, at 6:1 ratios, lowers the ridiculous "breakeven" prices analysts like to use to make it seem that shale oil is profitable at any price over $40, or $30, or whatever stupid stuff the shale oil industry lays claim to that week. The lower the price of oil goes the lower reported breakeven prices go, for some odd reason. I have yet to sort that out.

If you don't think oil wells in the Permian are getting gassier, this also from Shale Profile Analytics, above, 2016 vintage wells now have 5.1 GOR ratios. As you can see in the same chart early vintage wells are over 6:1 GOR, some pushing 7:1.

One final "salute" to BOE, it makes estimated ultimate recovery (EUR) look REALLY good. Using data from gazillions of wells it's pretty possible to predict rising GOR and model some stunning BOE EUR type curves accordingly. It's the stuff investor presentations are made of and lenders eat it up. The vogue claim now in the Permian Basin is 1.5MM BOE EUR's, 70% of that being oil. At first. By the time that 1.5MM BOE might actual be realized, twenty years down the road, that barn burner "oil" well is making 70% gas and is no longer an oil well, it's a gas well.

You'd think as important as associated gas is to Permian operators, to well economics and to promoting the Permian 'revolution" they'd want to do something more with that gas than piss it off up a flare stack, uh? Rystad, however, now says Permian flaring exceeds 750MMCFPD, which means it's actually, in real life a BCF or more, easy.*

The E in BOE; up, up and away.